Markup Subsidy and Risk Sharing Scheme

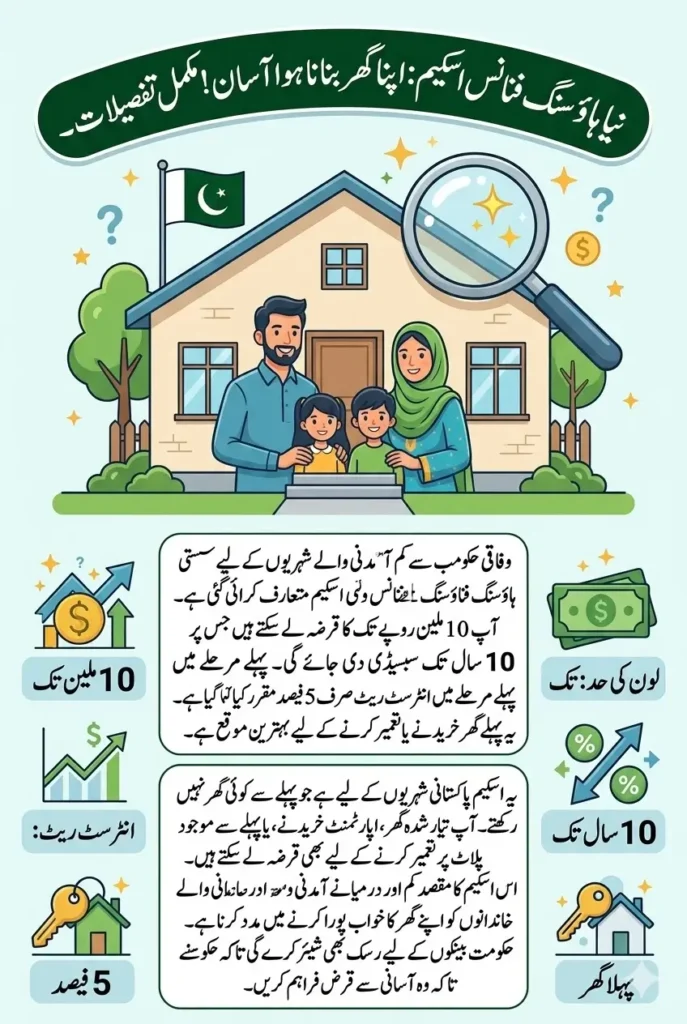

The federal government has introduced important revisions to the Markup Subsidy and Risk Sharing Scheme for Affordable Housing Finance to make homeownership more accessible for low- and middle-income citizens. The updated framework was approved by the Economic Coordination Committee (ECC) and later ratified by the federal cabinet to strengthen affordable housing opportunities across Pakistan.

This initiative is designed to support individuals who want to buy or build their first home but face financial barriers. By offering subsidized financing and reducing risk for banks, the government aims to expand access to housing loans and encourage financial institutions to participate more actively in the housing sector.

KPK Ramzan Relief Package 2026: How to Apply & Check Eligibility

Eligibility Criteria for the Affordable Housing Finance Scheme

The eligibility requirements under the scheme remain the same even after the recent revisions. The facility is specifically intended for first-time homeowners who are Pakistani citizens and possess a valid Computerized National Identity Card (CNIC). Applicants must also confirm that they do not already own any residential property in their name.

This requirement ensures that the benefits of the program reach individuals who genuinely need housing assistance. By focusing on first-time buyers, the government is targeting families that have previously been unable to purchase or construct their own homes due to financial limitations.

pmrrp.nitb.gov.pk PM Ramzan Package 2026 – CNIC Eligibility Check Complete Guide

Housing Options Covered Under the Scheme

The revised Markup Subsidy and Risk Sharing Scheme for Affordable Housing Finance allows multiple housing options for borrowers. Applicants can obtain financing for purchasing a ready-built house or apartment, constructing a house on an already owned plot, or buying a plot followed by house construction.

This flexibility enables families to choose the option that best suits their needs and financial situation. It also promotes growth in both the construction sector and the real estate market, helping stimulate economic activity related to housing development.

Approved Housing Unit Sizes

Under the scheme, the government has defined limits for housing units to ensure that financing is directed toward affordable housing projects. The approved size for houses is up to five marla, while flats or apartments can be financed up to a maximum size of 1,500 square feet.

These size restrictions are designed to focus the scheme on smaller housing units that are typically affordable for middle- and lower-income households. The policy also ensures that the program remains targeted toward genuine housing needs rather than luxury real estate investments.

| Housing Type | Maximum Size Allowed |

|---|---|

| House | Up to 5 Marla |

| Flat/Apartment | Up to 1,500 Square Feet |

9999 PM Ramzan Package 2026 Registration and CNIC Status Check Complete Guide

Participating Financial Institutions

A wide range of financial institutions will participate in the implementation of this housing finance program. These include commercial banks, Islamic banks, microfinance banks, and the House Building Finance Company Limited (HBFCL).

By involving multiple banking institutions, the government aims to expand the availability of housing loans across the country. This collaborative approach allows borrowers to access financing through various channels while ensuring that banks remain actively engaged in supporting affordable housing initiatives.

Key Features of the Revised Housing Finance Scheme

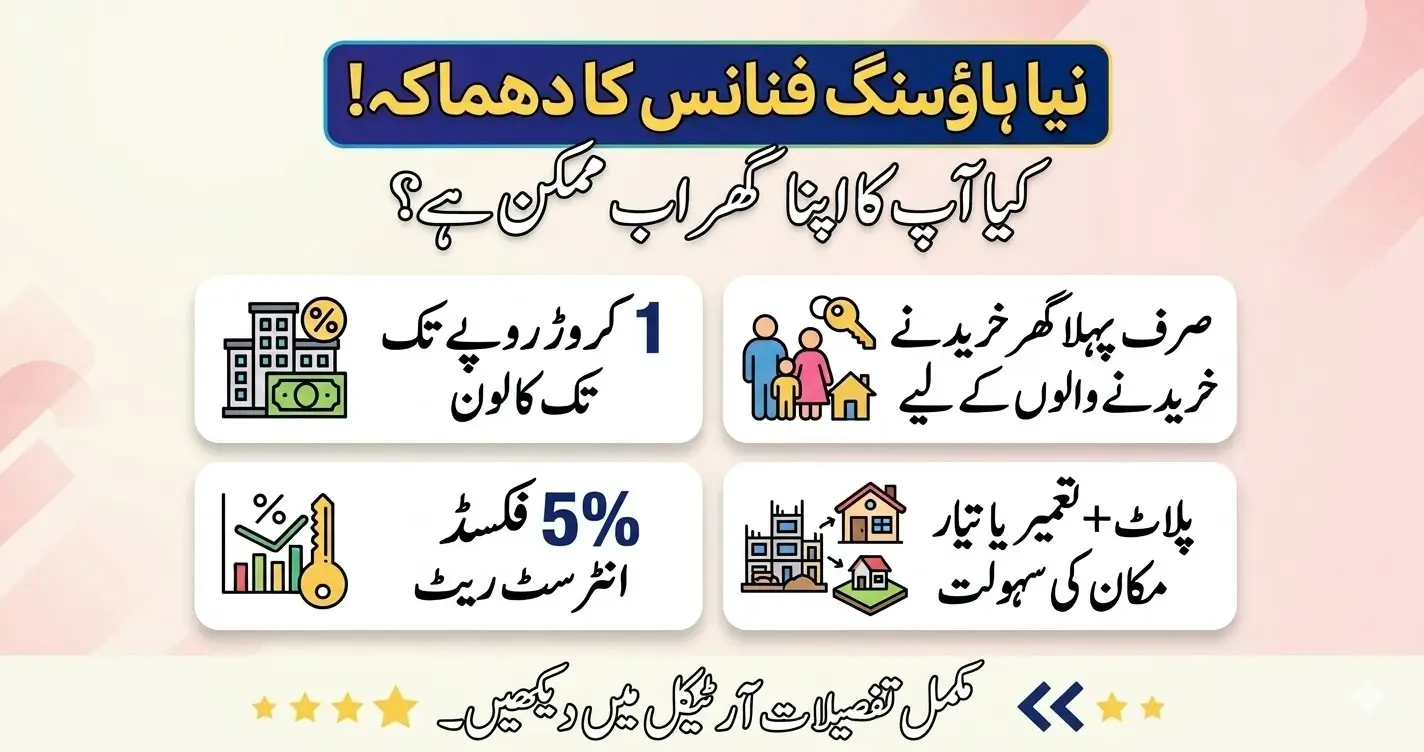

- The maximum loan limit increased to Rs 10 million

- Government markup subsidy available for the first 10 years

The revised scheme significantly increases the maximum loan amount available to borrowers. Individuals can now obtain financing of up to Rs10 million, which will help more families afford housing in urban and semi-urban areas where property prices have increased in recent years.

Despite the increase in loan size, the maximum repayment period remains at 20 years. This longer repayment tenure reduces the monthly financial burden on borrowers and makes the housing loan more manageable for middle-income households.

Interest Rate Structure and Subsidy Support

Under the revised framework, the pricing for banks will be based on the one-year Karachi Interbank Offered Rate (KIBOR) plus three percent. However, borrowers will benefit from a fixed markup rate of five percent, which will remain consistent for both tiers of applicants.

Previously, Tier-2 borrowers had to pay a higher interest rate, but the government has now standardized the rate at five percent. This change ensures equal benefits for all eligible applicants and makes the scheme more attractive for prospective homeowners.

| Loan Feature | Details |

|---|---|

| Maximum Loan Amount | Rs10 Million |

| Loan Tenure | Up to 20 Years |

| Borrower Interest Rate | 5 Percent |

| Bank Pricing | One-Year KIBOR + 3 Percent |

| Government Subsidy Period | First 10 Years |

Maryam Nawaz 10000 Scheme Check Online – Complete Guide for Applicants

Loan-to-Value Ratio and Borrower Contribution

The loan-to-value ratio under the scheme remains set at 90:10. This means that banks will provide financing for 90 percent of the property value, while the borrower will contribute the remaining 10 percent as equity.

Such a financing structure significantly reduces the upfront financial requirement for buyers. As a result, many families who previously could not afford a large down payment can now take advantage of affordable housing finance opportunities.

Government Risk Sharing for Banks

- The government will cover 10 percent of the outstanding portfolio as first-loss risk

- This encourages banks to provide more housing loans

To encourage financial institutions to participate in the scheme, the government has introduced a risk-sharing mechanism. Under this arrangement, the government will provide risk coverage for up to 10 percent of the outstanding housing finance portfolio.

This first-loss coverage reduces potential financial risks for banks and increases their willingness to offer housing loans to eligible applicants. The policy is expected to expand the overall availability of affordable housing financing across the country.

Target to Finance 500,000 Housing Units

The government has set an ambitious target to finance 500,000 housing units over the next four years. The plan outlines a gradual increase in the number of financed units each year.

| Fiscal Year | Target Housing Units |

|---|---|

| 2025–26 | 50,000 |

| 2026–27 | 100,000 |

| 2027–28 | 150,000 |

| 2028–29 | 200,000 |

This phased approach allows financial institutions and housing authorities to gradually scale up their operations. It also ensures that infrastructure and administrative systems remain capable of supporting the increasing demand for housing finance.

Mera Ghar Mera Ashiana Loan Scheme 2026 – Apply Online, Eligibility & Latest Updates

Role of the State Bank of Pakistan in Implementation

The State Bank of Pakistan (SBP) will serve as the implementing agency responsible for overseeing the scheme. It will coordinate with the Pakistan Housing Authority-Foundation and participating financial institutions to ensure smooth execution.

The SBP will also monitor lending activities, maintain regulatory oversight, and ensure that banks follow the guidelines established under the program. This supervision is essential to maintain transparency and ensure that the scheme benefits the intended target group.

Adjustment of Interest Rates for Existing Borrowers

The notification issued by the Ministry of Housing and Works also includes relief for borrowers who have already received loans under the earlier version of the scheme. Loans previously disbursed at an interest rate of eight percent will now be adjusted to five percent.

This adjustment ensures fairness and uniformity among all borrowers participating in the program. By reducing the interest rate for existing loans, the government has extended the benefits of the revised policy to those who joined the scheme earlier.

Benazir Taleemi Wazaif New Update: Latest Payment Schedule & Student Eligibility

FAQs

What is the Markup Subsidy and Risk Sharing Scheme for Affordable Housing Finance?

It is a government initiative designed to provide affordable housing loans with subsidized interest rates for first-time homebuyers in Pakistan.

Who is eligible for this housing finance scheme?

Pakistani citizens with a valid CNIC who do not own any house or apartment in their name can apply for the scheme.

What is the maximum loan amount available under the scheme?

The revised policy allows borrowers to obtain housing finance of up to Rs10 million.

What interest rate will borrowers pay under the scheme?

Eligible borrowers will pay a fixed interest rate of five percent while the government provides markup subsidy for the first ten years.

How much down payment is required for the loan?

Borrowers must contribute 10 percent of the property value, while banks will finance the remaining 90 percent.